Highlights for cattle

- Cattle prices are likely to remain mostly stable throughout the next month, with increased supply being met by strong demand.

- Slaughter rates are forecast to remain stable, with processing centres reported to be booked out well in advance and an abundance of stock available on local markets to purchase.

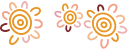

Australian cattle prices have recorded moderate growth throughout October. The National Young Cattle Indicator (NYCI) increased 12.8 per cent month-on-month, presently sitting at 338c/kg. This is also 67.4 per cent higher than a year ago when the market was at record lows. However, despite this growth, current price levels are still comfortably 21.6 per cent below the five-year average. The uplift in prices mainly observed at the beginning of October came on the back of continued strong export demand. This was in particular from the US. The outlook for November is to see stability in pricing. With the recent dry conditions in southern regions, supply levels have increased at local markets. This has resulted in southern buyers who were purchasing stock from northern markets returning to local markets. However, with most processing centres being booked out well in advance now into late November or near the end of 2024, demand for stock may soften. This equilibrium was observed throughout the last week of October. This is where prices remained mostly stable, and it is likely to continue throughout November.

National weekly slaughter rates remained stable during October. This was at just under 140,000 head on average. There was a strong supply of cattle on local markets. National cattle yardings were 14.1 per cent above the average for 2024 in October. This provided processing centres with sufficient stock levels. Looking from a national perspective, year-to-date cattle slaughter is presently 15.7 per cent higher than 2023. The increase in processing can be attributed to an uplift in female slaughter. NSW and QLD processing of female cattle has seen significant change. There have been rises of 22.2 and 27.1 per cent respectively. This when compared to more modest changes of male slaughter -4.7 per cent and 9.5 per cent in both states respectively further illustrates that female slaughter is the primary driver for in the increase in volume processed during 2024. Slaughter is forecast to remain mostly stable throughout November. It is expected that with additional shifts being added to manage extra stock, slaughter rates should remain at around 140,000 head per week Processing centres are mostly booked out for November, with some stocked until the end of the year. Additionally, cattle supply is unlikely to be an issue in coming months, supporting the notion of steady slaughter rates.

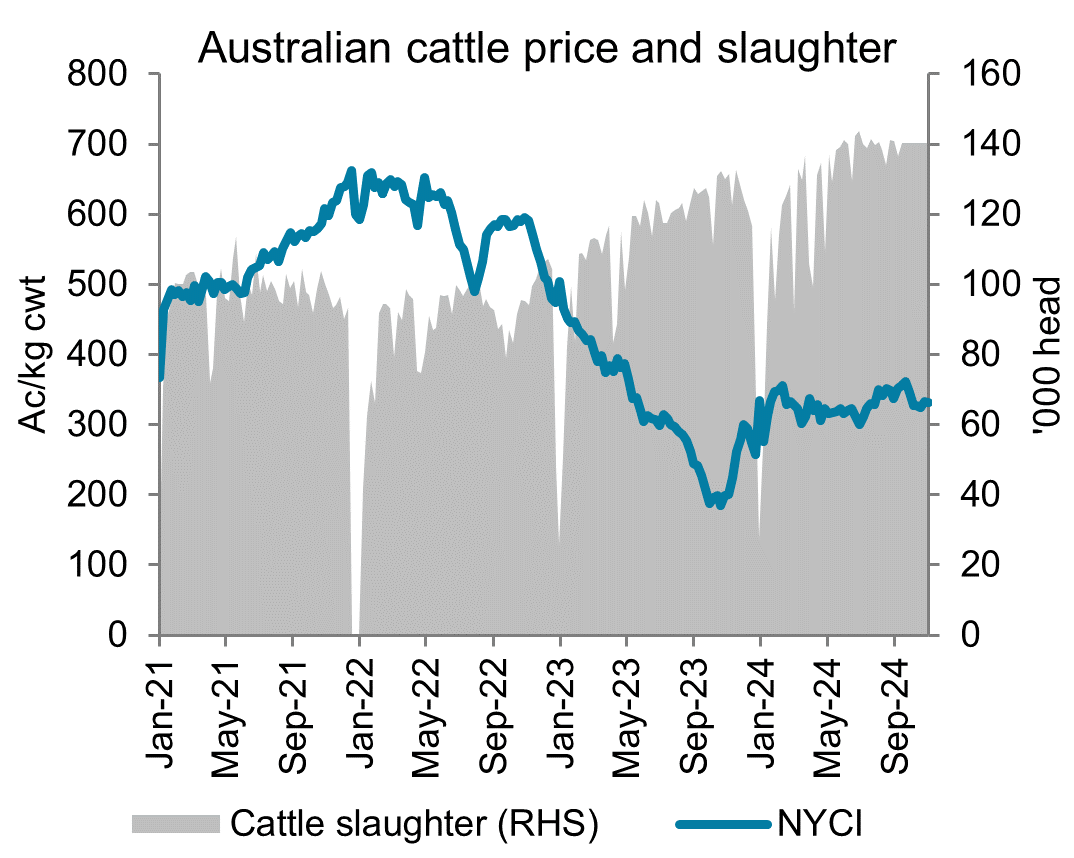

Australia’s beef exports soared to just over 130,000 tonnes in October. This is now the strongest monthly level on record, breaking the previous record set in July this year. The extraordinary volume of beef transported can be attributed to a boost in exports to the US. Exports to the US increased 21.9 per cent month-on-month, to just under 45,500 tonnes. The second largest market for October was South Korea at 19,733 tonnes. This demonstrates just how strong exports to the US were compared to other key markets. Year-to-date US exports presently sit 66.5 per cent greater than 2023. The significant demand from the US has left total beef exports 24.4 per cent greater year-to-date than 2023 and 49,8 per cent higher than the five-year monthly average. Export volume to Japan softened this month. Tight economic conditions and softer Japanese consumer spending weakened demand. Despite a 12.2 per cent decrease month-on-month, exports are still 24.8 higher year-to-date than 2023. Exports are forecast to marginally decline throughout November. During the next month, there will be an implementation of a doubling in tariffs due to the safeguard provisions under FTA’s with Australia. The tariffs will be implemented on Australian exports to China, Japan and South Korea as a safeguard market protection provision. This is likely to result in reduced exports to these destinations for the remainder of 2024.

Bendigo Bank Agribusiness Insights publication(s) are for information purposes only and contain unsolicited general information, without regard to any individual objectives, financial situation or needs. Please refer to the terms and conditions.

Related Articles

-

April's cattle market update

Australian cattle prices recorded moderate growth again throughout March with prices peaking in the final week of the month. -

March's cattle market update

Australian cattle prices recorded moderate growth throughout February. The NYCI saw a 17 per cent increase month-on-month. -

February's cattle market update

Australian cattle prices recorded a mixed beginning to 2025. The NYCI burst out of the blocks in the first few weeks of January, peaking at 379c/kg.